- /

What Inflation and Elevated Mortgage Rates Mean for Johnson County Home Buyers

Inflation is running above the Federal Reserve's target. That matters for mortgage rates, and mortgage rates matter for everyone thinking about buying or selling in 2026. Here is what the data actually shows, and what it means for buyers and sellers in Johnson County.

The Inflation Number the Fed Is Actually Watching

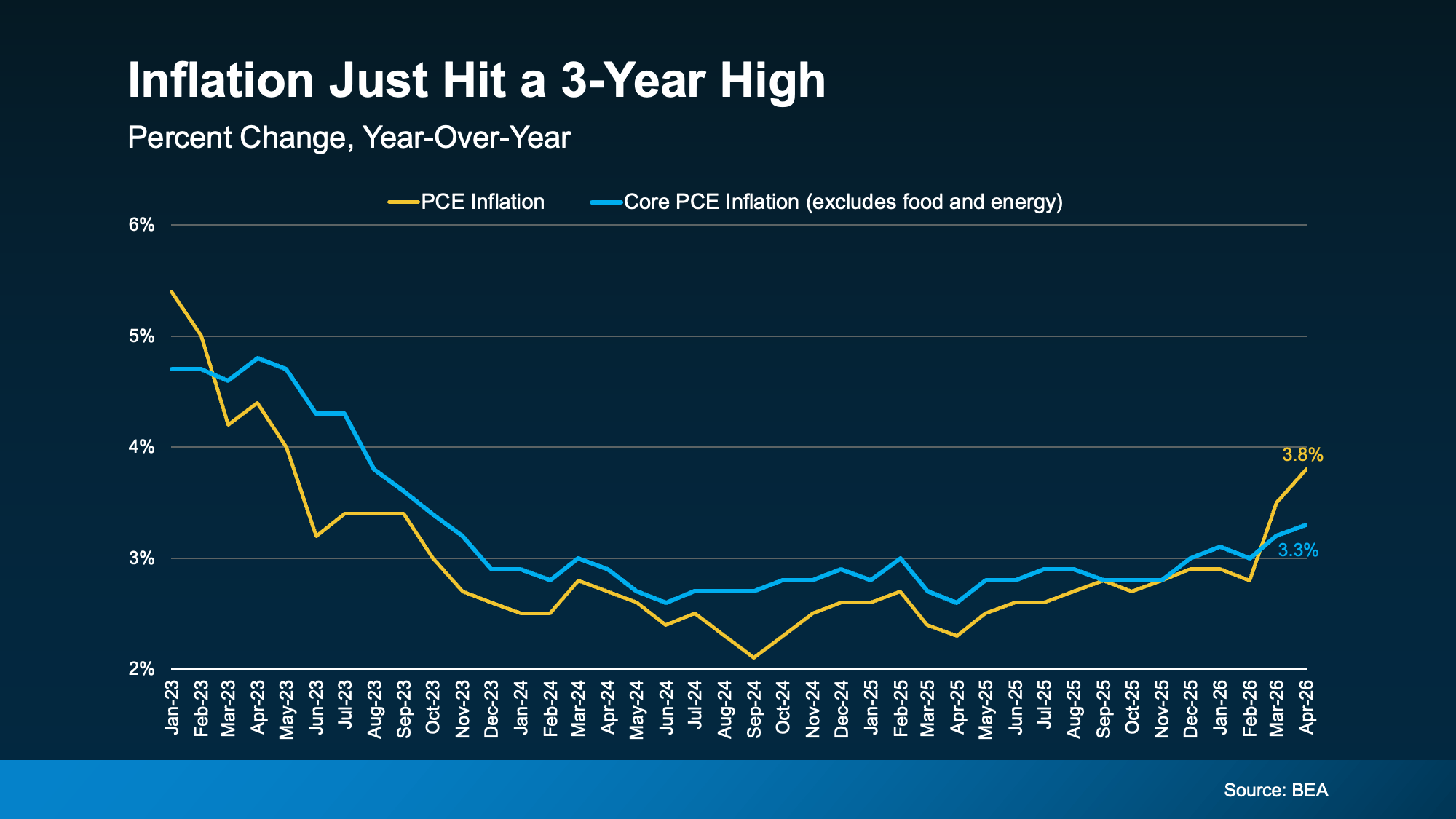

The federal government tracks inflation through two versions of PCE — the Personal Consumption Expenditures Price Index, which measures how much more consumers are paying for goods and services year over year. Overall PCE has moved higher since February, with energy and gas prices a significant contributor, driven in part by the ongoing conflict in the Middle East.

The Federal Reserve, however, watches core PCE, which strips out energy and food prices due to their volatility. Core PCE is also rising, but at a slower pace than the headline number. That distinction matters. If the inflation spike is primarily energy-driven and geopolitical, it may moderate when those conditions change. If it were embedded in core prices across the economy, the outlook for rate relief would be considerably dimmer.

What Elevated Inflation Means for Mortgage Rates in Johnson County

The Fed's response to elevated inflation is to hold rates higher for longer. That policy has kept mortgage rates in the 6.5% range through mid-2026, above what was projected at the end of 2025. Meaningful rate relief is not arriving this year.

At the Johnson County median price of $485,000 with 20% down, the difference between a 6.0% rate and a 6.5% rate is approximately $155 per month on a 30-year fixed mortgage. That is real money. It is not the spread that separates financially qualified buyers from the market. What separates buyers right now is hesitation — the assumption that waiting for rates to fall will improve their position.

In a market where Johnson County inventory is down 8.8% year-over-year and homes are selling for 101.3% of list price in an average of 30 days, waiting for rates to move while prices continue climbing is the trade most buyers are unknowingly making.

Why This Is Not a 2008 Situation — Especially Not in Johnson County

The 2008 housing collapse was driven by specific conditions that do not exist today: a flood of distressed inventory, loose underwriting standards, and homeowners with no equity. Lending standards today are far stricter. Two-thirds of homeowners nationally carry at least 50% equity. There is no distressed seller wave building.

In Johnson County specifically, the profile is even further removed from 2008. Supply sits at 2.0 months. Year-to-date closed sales are up 8.5% compared to this time in 2025. The average seller is receiving 101.3% of original list price. Those are not the numbers of a market under stress. Affordability is the current challenge. Affordability and instability are not the same thing.

What Buyers and Sellers Should Do in This Environment

For buyers, rate buydowns, adjustable-rate products, and seller-paid concessions are all tools worth discussing with a lender. The relevant question is not when rates will drop. It is whether the purchase makes sense under current conditions — and what the specific financial picture looks like at Johnson County price points with a rate in the mid-sixes.

For sellers, the Johnson County market continues to reward well-priced, well-presented homes. Sellers waiting for rates to fall before listing — on the assumption that buyers will flood back the moment rates drop — are also waiting to face increased competition from other sellers with the same idea.

Christopher Munkel tracks Johnson County market conditions month over month through Heartland MLS data. Translating national inflation and rate dynamics into specific decisions for buyers and sellers in Johnson County is the work Munkel Real Estate Solutions does in every client conversation.

Market data sourced from Heartland MLS and KCRAR FastStats, May 2026.

Categories

- All Blogs (91)

- affordability (18)

- Agent Value (3)

- Buying Tips (27)

- Downsize (4)

- economy (12)

- equity (11)

- Expired/Withdrawn/Cancelled (5)

- Featured (1)

- First-Time Buyers (25)

- For Buyers (64)

- For Sellers (50)

- Forecasts (10)

- foreclosures (1)

- Home Prices (22)

- Inventory (11)

- Mortgage Rates (14)

- Move-Up (4)

- New Construction (5)

- Overpricing (3)

- Price it Right (2)

- Rent vs. Buy (5)

- Selling Tips (21)

- Senior Market (2)

Recent Posts

Founder & Principal | Munkel Real Estate Solutions | License ID: KS#00251082 | MO#2024042017

+1(913) 490-6011 | chris@munkelrealestatesolutions.com